Let’s Get Started!

Quick Loan Links

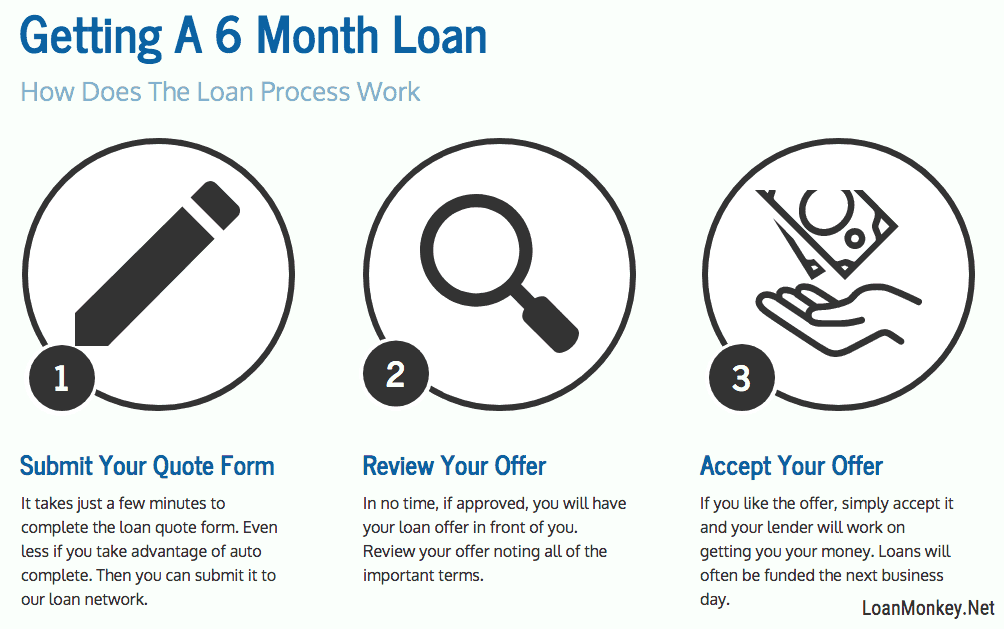

Fast Online Loan Quote – About Installment Loans – Compare – Bad Credit Loans

6 Month Loans

The term payday loan refers to a loan that is due on your payday. Because of this, a payday loan is a loan with a term of about 2 weeks. A loan with such a short term can make it difficult when you are trying to cope with an emergency and get your finances back on track.

An installment loan, on the other hand, is a loan that can be stretched out to a longer term. So, if you need a loan of a longer length, what you are really looking for is an installment loan. The loan term will vary based on how much you borrow and your credit but they can certainly be had in the 6 month varieties. In general, installment loans come in 3 month terms, all the way up to 6 year terms.

Why Choose An Installment Loan?

The primary reason that you would choose to go installment over payday is that it is a longer term loan. When a financial crisis occurs, 2 weeks is hardly ever enough time to get things back to normal. This is why people get into trouble with a payday loan. They take one out and it is due in just a few weeks. This does not give them time to handle their finances and they find that they can not afford to pay back the loan when it is due. Their only solution is to extend the loan or take out another one. This costs more fees and starts the payday loan cycle. By the time they finally get the money paid off, many will have paid double the amount of the loan in fees alone.

With an installment loan, your lender will divide out your payments over a much longer term, in this case six months. This gives you more time to handle your situation. It also makes the payments much smaller. Instead of having to come up with one huge lump sum, you only need to pay back a portion at a time.

Lastly, fees are often much less with an installment loan versus a payday loan. With payday loans, the lender will charge a lump sum fee per $100 borrowed. This can result in an effective APR in the 400% range. Installment loan interest rates are typically much lower and your credit rating will be taken into account which can qualify you for a better rate.

Qualifying For A 6 Month Installment Loan

Loans are available for those with all types of credit so do not prejudge yourself. Even if you have some dings on your report, you can qualify. In general, you must have a source of income, a checking account and good contact information. Beyond that, every lender in our network will have slightly different qualifications. That is the beauty of dealing with a lender network instead of a single individual lender.

With an individual lender, you must meet one particular set of criteria. If you do not fit into their mold, you get denied. With a network, if one lender does not want to work with you, your information just goes securely to the next lender. This happens again and again until a lender is found that wants to make you an offer. It is the quickest way to get an approval and if time is of the essence, it is the best way to go.

Payday Or Installment

There is a huge difference between these two loan types. Let’s take a look at what each loan looks like and the pros and cons of both. You will no doubt see right away that an installment loan is the right choice for you.

Payday Loans

- Due In About 2 Weeks

The name of the loan comes from the fact that it is due to be repaid on the borrowers next payday. In most cases, this is 10 to 14 days. The loan can often be extended but fees will apply and they can be high. 6 month payday loans do not really exist. - Small Dollar Loans

Loans are capped by state rules. The most you can take out is $1000, depending on the state that you live in. Some states have limits that are even lower. Because of the short loan term, the less you borrow the better. - Not Available Everywhere

Some states do not allow payday loans because of the fees involved and past behavior of lenders. - One Payment

When the loan is due to be repaid, the borrower must pay the loan back all at once. This payment will include all principal and loan fees. Lenders will automatically deduct the amount from your account in most cases.

As you can see, there are some major drawbacks to a payday loan with one of them being that they are not available for six months. You can only borrow a limited amount of money, you must pay the loan back quickly, you must pay it back all at once and they may not be available in your state. On the plus side, these loans are super easy to qualify for.

Installment Loans

- Multiple Month Terms

Installment loans, as the name implies, are paid back in installments. Loan terms will be set so that the borrower can take three months or longer to pay the loan off. This can make it easier to get finances in order after an emergency. - Higher Loan Amounts

Loan amounts are not capped at small dollar amounts. Our lenders, for example, may be able to lend you up to $50,000. - Greater Availability

Loans are not subject to the restrictions of payday loans so you are more likely to be able to obtain one. - Multiple Payments

You can break the payments up over a longer term, resulting in smaller and more manageable amounts.

It is easy to see that installment loans are much more user friendly. You can get terms of 6 months or more, you can get more money, they are more available and of course, they have smaller and more manageable payments. Loans are subject to credit approval but if you qualify for an installment loan, it will probably be far more beneficial to you than a payday loan.

Bad Credit Loans

Even with bad credit, you may qualify for a loan from one of our lenders. Many of them specialize in working with credit types that are less than perfect.

If you have bad credit, you have probably searched for “no credit check” loans. Truth is, these do not exist. ALL lenders run some sort of credit check. If they didn’t, they would not be in business for long.

Just because you have bad credit does not mean that you should be afraid of the credit check. Many of our lenders specialize in this market and may be prepared to give you a loan offer for 6 month loans or even longer.

Stop settling for a regular payday loan and get the added convenience of an installment loan. Do remember though that even a 6 month payday loan is a short term loan and it should not be used lightly. These loans should be used only for emergencies and you should always look at your other loan alternatives.